Description

*Strategy signals are emailed daily, prices are USD charged monthly.

Strategy Overview: US Stocks Alpha

This systematic strategy utilizes a bifurcated approach to trade the constituents of the SPX (S&P 500), RUI (Russell 1000), and NDX (Nasdaq-100). By running two distinct sub-strategies simultaneously, the model captures alpha in both trending and range-bound environments while utilizing a proprietary regime filter to dictate capital allocation.

Core Methodology

The strategy operates on two primary quantitative engines:

-

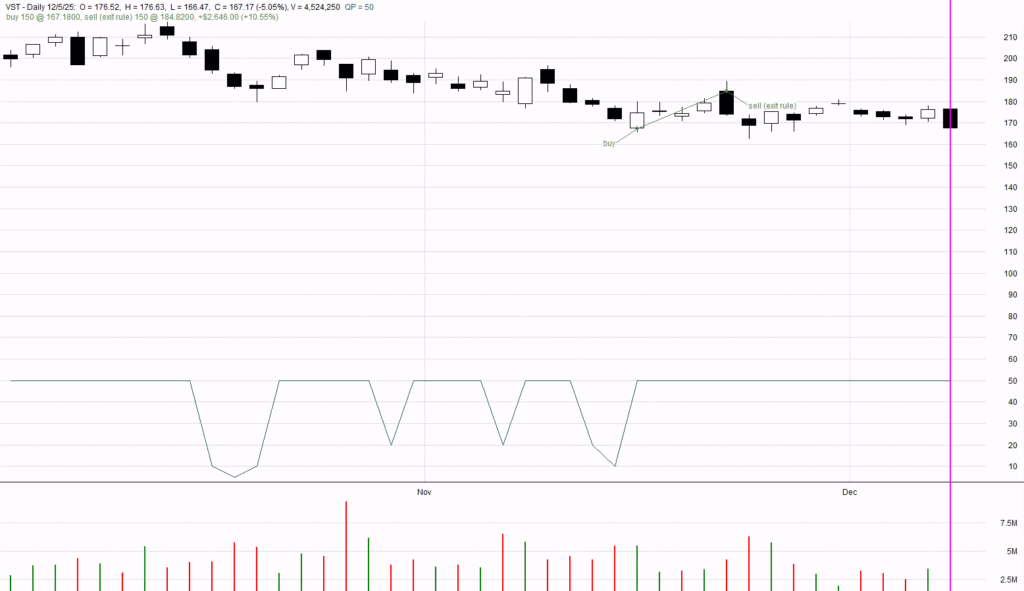

QP (Quantitative Price) Mean Reversion: Designed for “overextended” markets, this engine identifies high-quality constituents that have deviated significantly from their short-term intrinsic price mean. It enters positions on technical exhaustion, betting on a rapid return to equilibrium.

-

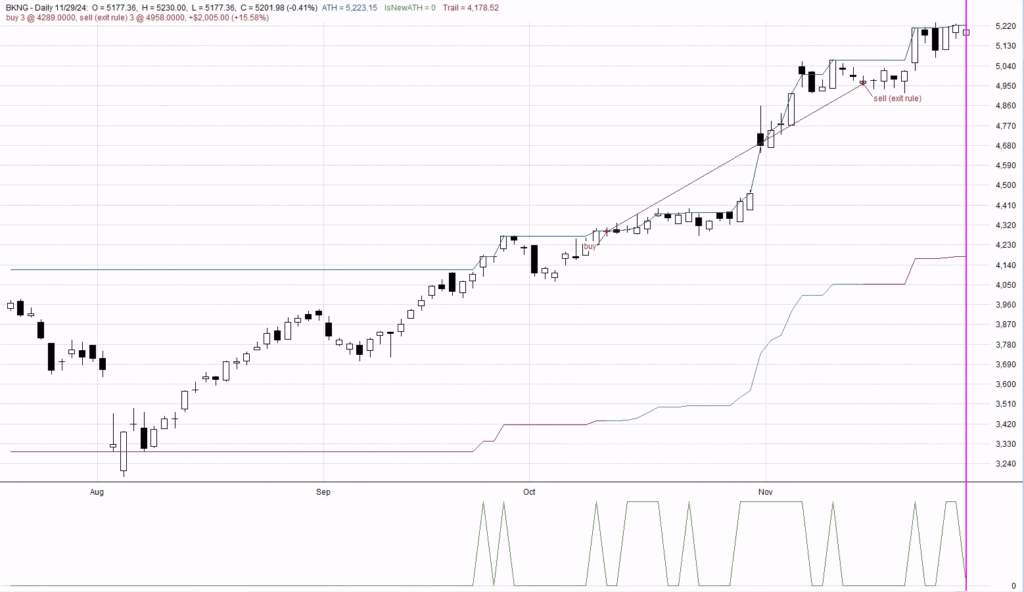

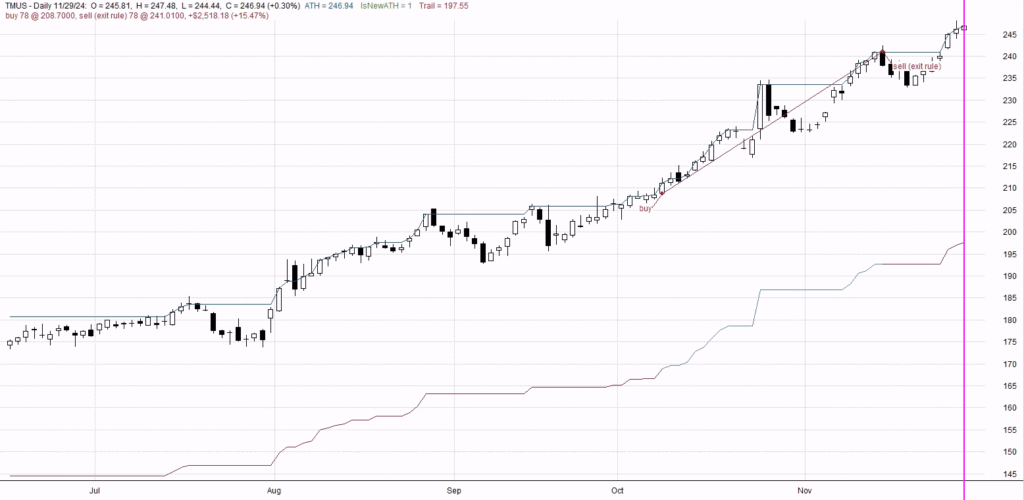

All-Time High (ATH) Momentum: This engine targets “blue sky” breakouts. It identifies stocks showing extreme relative strength that have cleared historical resistance. It capitalizes on the momentum effect and the lack of overhead supply to capture accelerated price appreciation.

The Volatility Regime Filter

The cornerstone of the strategy’s low-drawdown profile is its Robust Regime Filter. Instead of trading blindly, the model analyzes market-wide volatility (VIX) and internal dispersion to classify the environment:

-

Low Volatility (Quiet): Increases exposure to the ATH Momentum engine.

-

High Volatility (Turbulent): Pivots toward Mean Reversion or shifts to cash/defensive postures.

Strategic Advantages

-

Diversified Alpha: By combining momentum (ATH) with mean reversion (QP), the strategy avoids the “style drift” traps that plague single-factor models.

-

Institutional Universe: By trading only SPX, RUI, and NDX constituents, the strategy ensures high liquidity and minimal slippage.

-

Risk Mitigation: The regime filter acts as a “circuit breaker,” significantly reducing exposure during market regimes where technical signals become noisy or unreliable.

Portfolio Composition

| Component | Primary Driver | Market Condition |

| QP Mean Reversion | Statistical Exhaustion | Mean-reverting / Range-bound |

| ATH Breakouts | Trend Persistence | Bullish / Low-volatility |

| Regime Filter | Volatility Analysis | Risk Management Overlay |

Strategy Note: This dual-engine approach is specifically engineered to provide a “smoother” equity curve, as the gains from mean reversion often offset the pullbacks experienced by momentum stocks during minor market corrections.

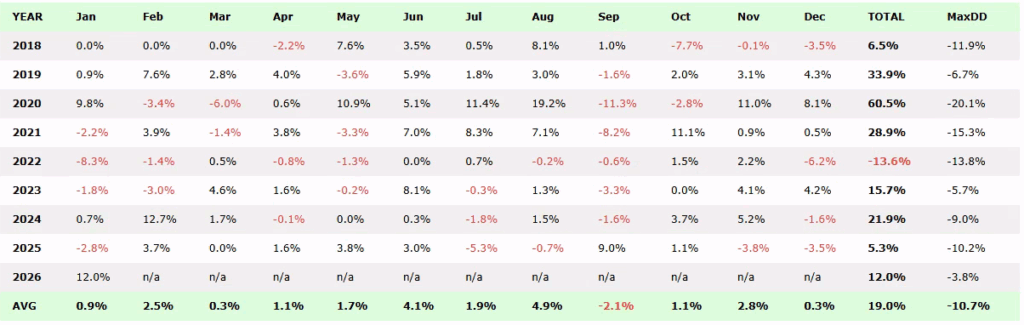

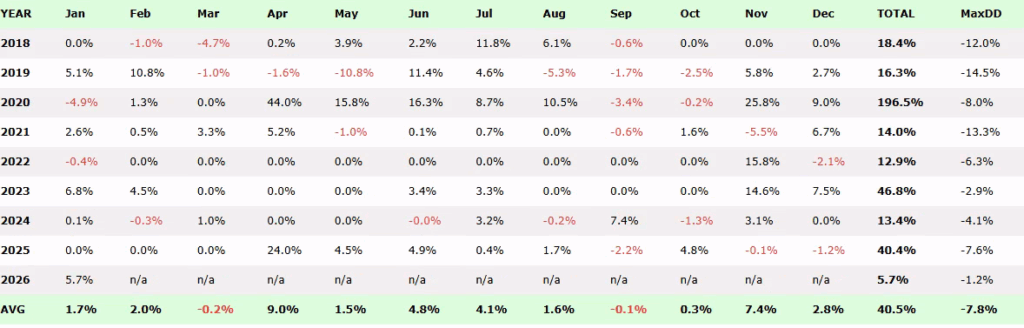

Key metrics

ATH

ROR: 20.32%

MaxDD: -20.12%

PctWins: 55.52%

QP Mean Reversion

ROR: 38.09%

MaxDD: -14.45%

PctWins: 51.70%

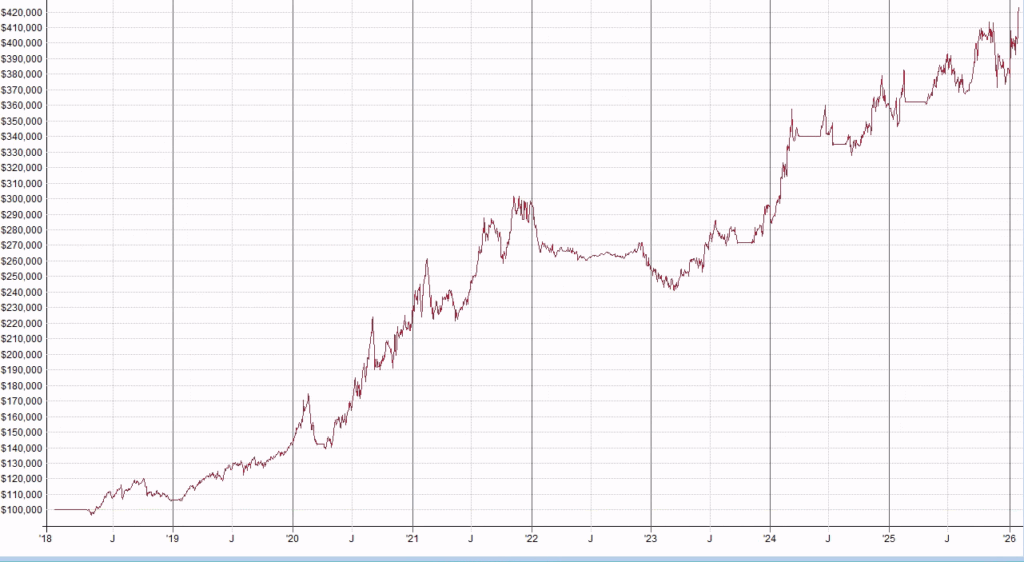

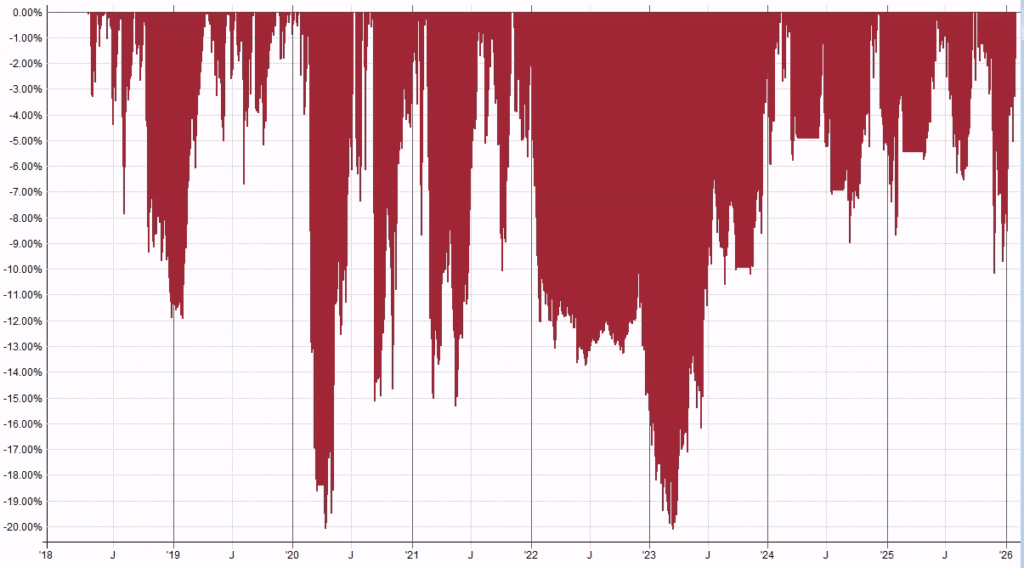

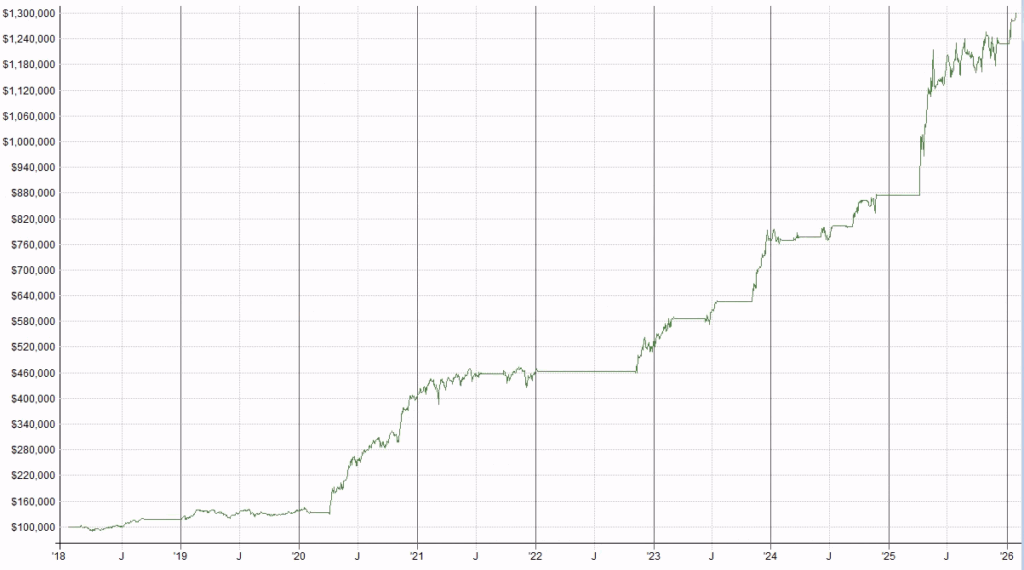

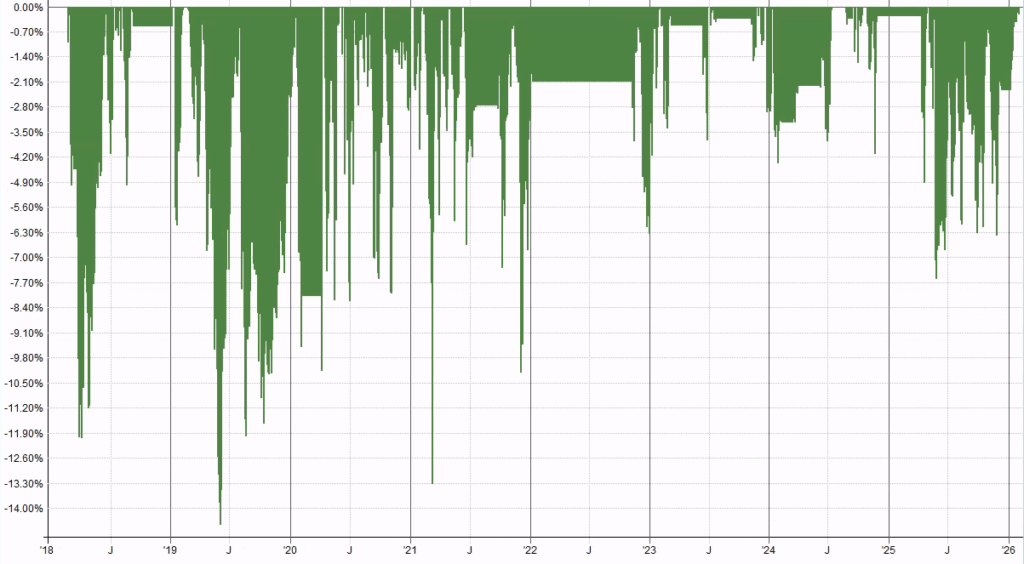

Performance charts

ATH

Equity

Drawdown

QP Mean Reversion

Equity

Drawdown

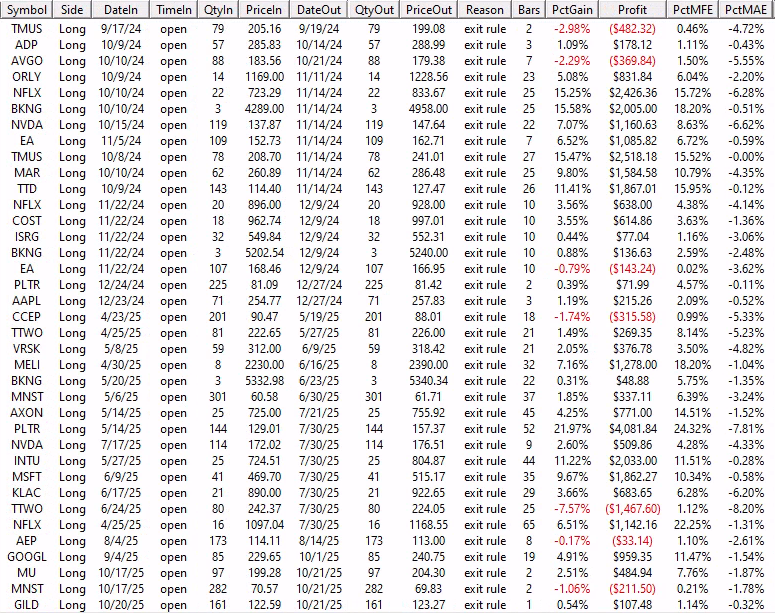

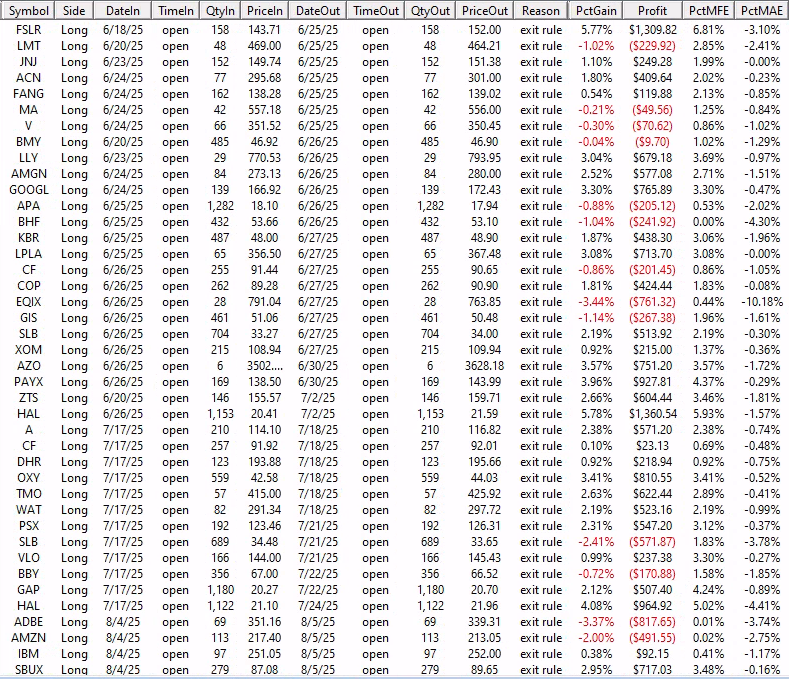

Sample Trades

Reviews

There are no reviews yet.